Financial Management Bond valuation

재무관리-채권평가

7-(3)

1. Treasury Quotes

Bond Quotes

매수가격(Bid)과 매도가격(Ask)

Bid price: 사려는 가격

Ask price: 팔려는 가격

따라서 항상

Ask price >> bid price

Bid-ask price

=매수가격(Bid)과 매도가격(Ask)의 차이

= 수익

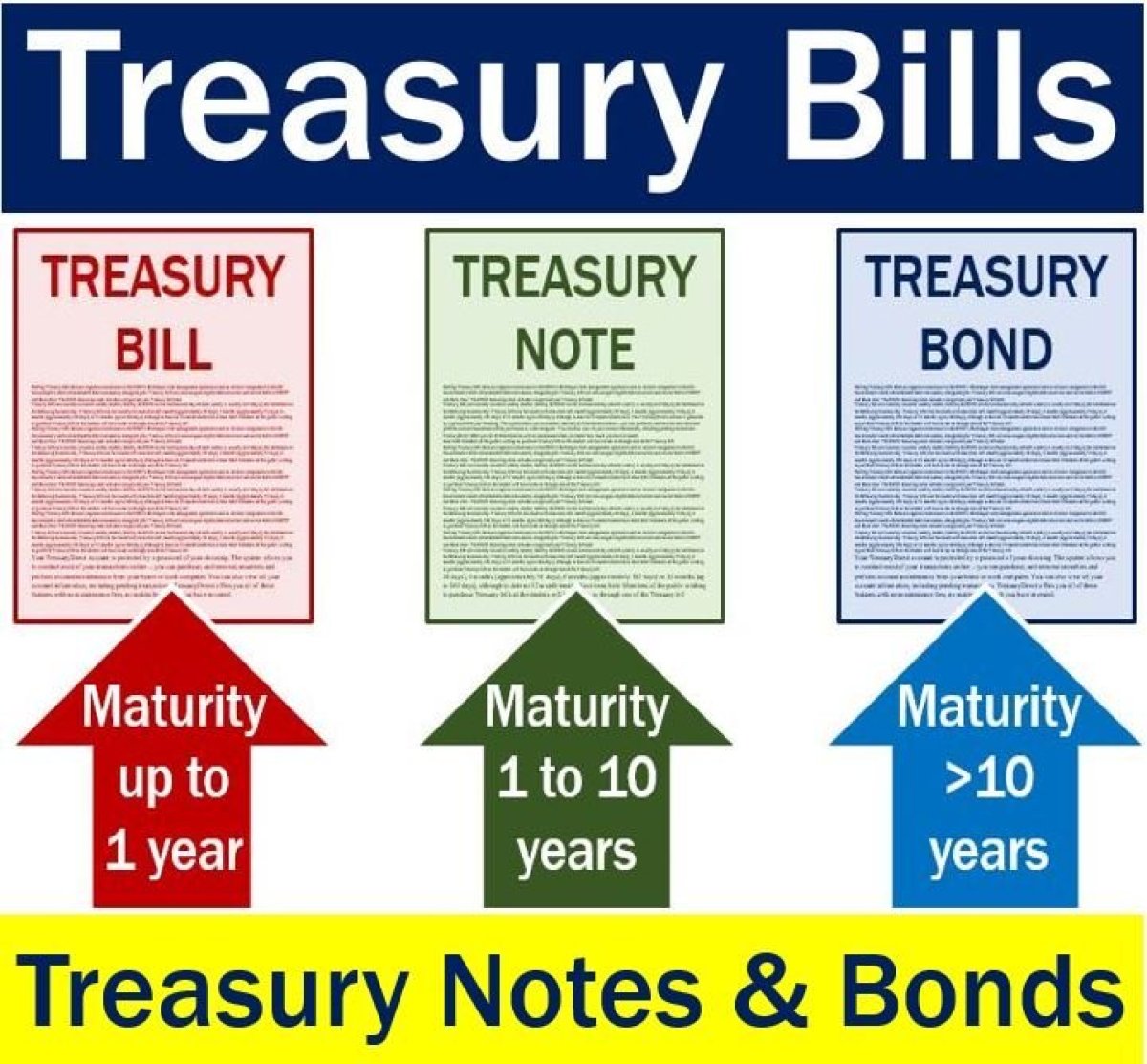

Treasury Bills :만기 1년이하 채권

Treasury Notes :만기 10년이하 채권

Treasury Bonds :만기 10년 초과 채권

2. Accrued interest.

금융에서 발생 된이자는 원금 투자 이후 축적 된 채권 또는 대출에 대한이자

또는 이전에 쿠폰 지급이 있었는지에 대한이자

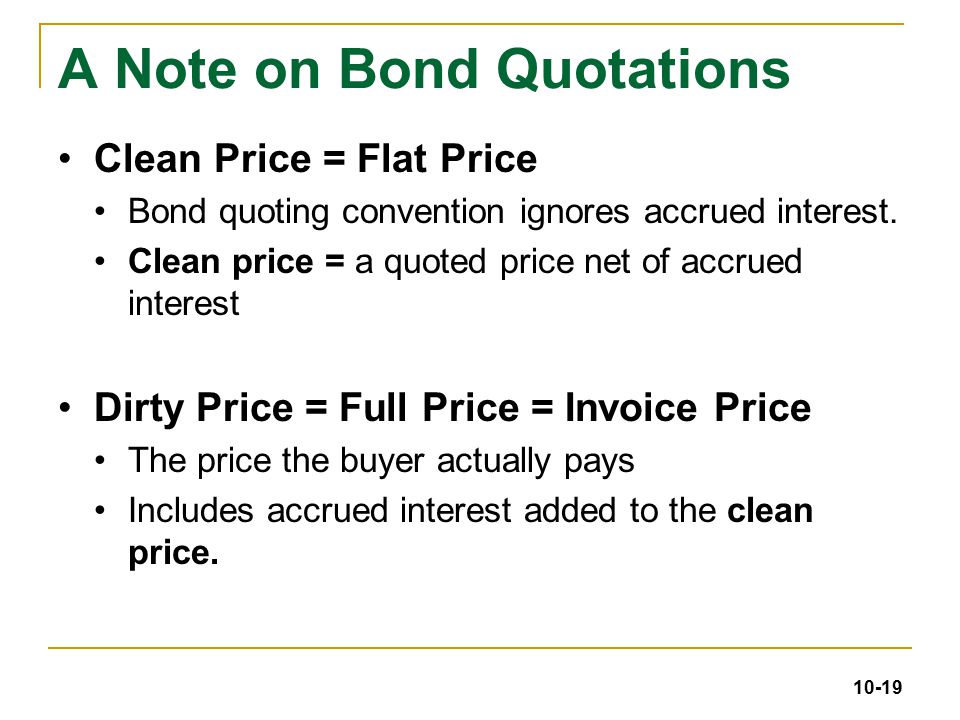

Invoice price= quoted price + accrused interest

ex) Bond of 1,000 @12% payable semi-annually

Quote=1,060

Two months since last coupon payment of $60

= there are four months to the next semiannnual coupon date

3. Zero- coupon bonds

제로쿠폰채권(Zero Coupon Bond)은

쿠폰금리 없이 발행가격을 이자에 의해 할인·발행하는 채권을 말한다.

상환기간까지 이자 지급이 없는 것이 특징으로

one-time payoff of the pricipal at maturity

제로쿠폰채권(Zero Coupon Bond)은

coupon이 없기 때문에 PMT는 필요없고

오직 FV, PV, I/Y 만 필요함-> chapter 5의 식이랑 똑같음

4. real vs nominal rate

real rate

인플레이션 영향 고려 O

구매력 & 투자자 자본

nominal rate

인플레이션 영향 고려 X

일반적으로 YTM 등등은 nominal rate를 기반함

inflation rate가 주어지면

nominal rate-> real rate 구할 수 있음

when real rates of interest are high,

all other rates tend to be high

<fisher effect>

(1+R)=(1+r)(1+h)

R= nominal rate : 명목 이자율

r= real rate: 실질 이자율

h= expected inflation rate : 인플레이션율

ex) If we require a 10% real return

and we expect inflation to be 8%,

what is the nominal rate?

*R=(1+r)(1+h)-1

(1+0.1) X (1+0.o8)-1=0.188=>18.8%

*대략값= r+h => 실질이자율 + 인플레이션율

10% + 8% =>18%

*Doing PV calculations with inflation

If you are using nominal dollars in cash flow-> nominal rate of return

If you are using real dollars in cash flow-> real rate of return

don't mix them up!

5. what determines the YTM

YTM= market discount rate

만기수익률(YTM; yield to maturity)

using to calcualte the future cash flow

maturity of a bond (long, short)

확실성 낮음, 높음

The yields fo trasury bills and bonds reflect term structure of interest rate.

<what determines the YTM?>

1) Time value of money,r =>oportunity cost

(basic structure of YTM)

2) expected inflation, h =>inflation premium

3) Interest rate risk premium

<other determinants of yields>

default risks premium: 파산위험 증가하면 YTM 증가

Taxability premium(discount):할인위험 증가하면 YTM 증가

Liquidity premium:유동성 증가하면 YTM 감소

나에게 안전한 채권이면 YTM 만기수익률은 감소

나에게 위험한 채권이면 YTM 만기수익률은 증가

YTM 과 price는 반비례!

만기수익률과 가격은 반비례!!

따라서

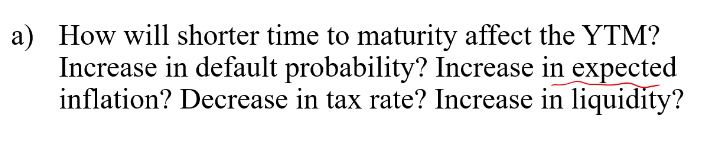

shorter maturity-> 굿 YTM 감소 -> bond price 증가

increase in default probability->배드 YTM 증가

increse in expected inflation ->배드 YTM 증가

decrease in tax rate ->굿 YTM 감소

increase in liquidity -> 굿 YTM 감소

'정보' 카테고리의 다른 글

| 코로나19 , 넷플릭스 그리고 OTT산업 (0) | 2020.05.20 |

|---|---|

| Financial Management -stock valuation (0) | 2020.05.20 |

| Financial Management -Bond valuation 채권평가 (0) | 2020.05.18 |

| [2020 인기 있는 여자 영어 이름] (0) | 2020.03.20 |

| [코로나/넷플릭스] 코로나 바이러스와 넷플릭스의 상관관계 (0) | 2020.03.20 |

댓글